The Greater Fool

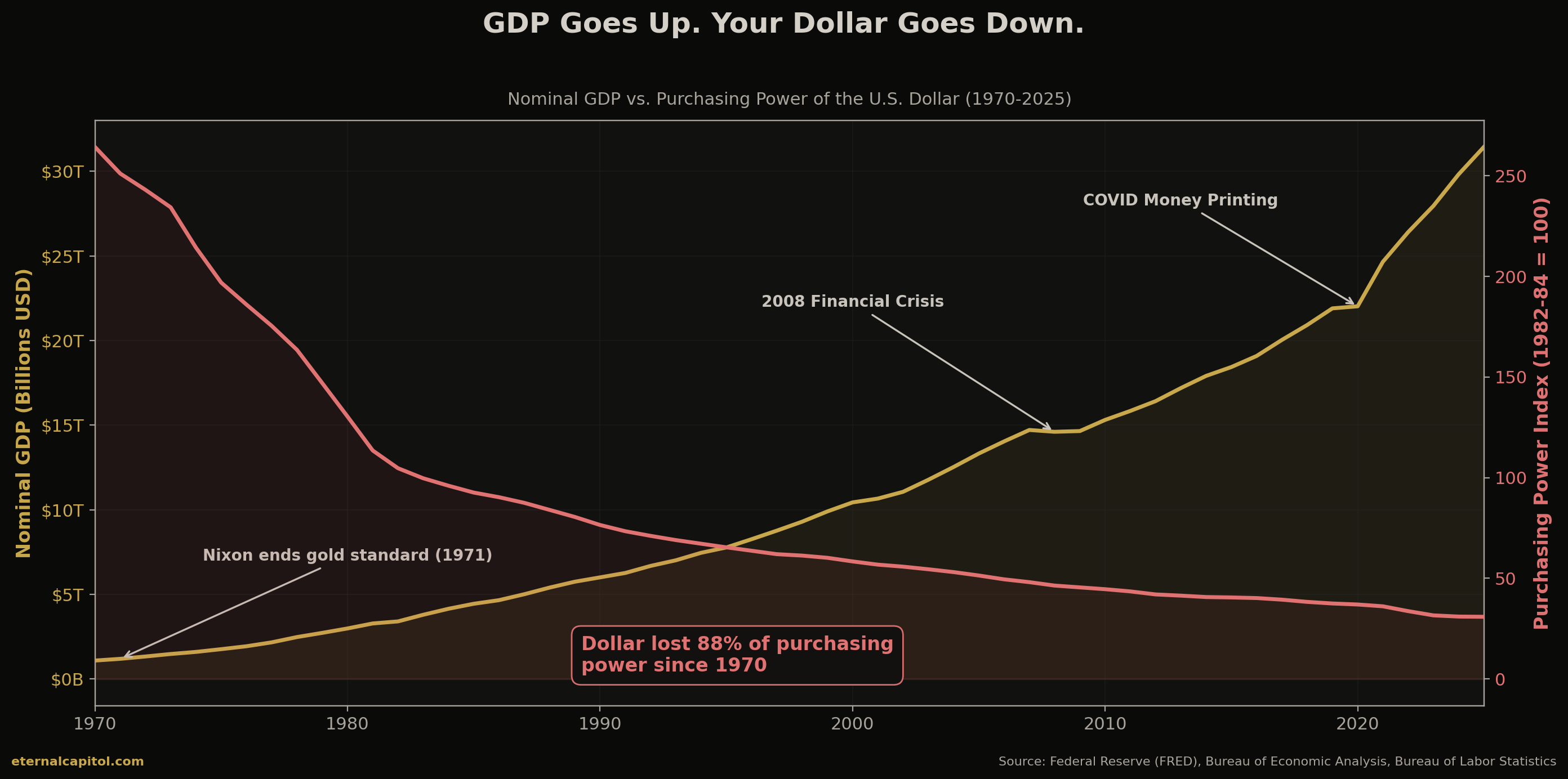

There's a con that's been running for over fifty years, and it doesn't matter which party sits in the Oval Office. Red tie, blue tie. The dollar in your pocket lost 88% of its purchasing power since 1970, according to the Bureau of Labor Statistics. Every president since Nixon has presided over that decline. Every single one.

Source: Federal Reserve (FRED), Bureau of Economic Analysis, Bureau of Labor Statistics

Look at that chart. GDP climbs from $1 trillion to $31.4 trillion. Politicians wave it around like a trophy. "The economy is growing." Sure it is. In nominal terms. Measured in a unit they keep making worth less. Your grandparents' dollar bought 3.3 times what yours does today. The economy didn't grow 30x in real output. The measuring stick shrank.

Same Team, Different Jerseys

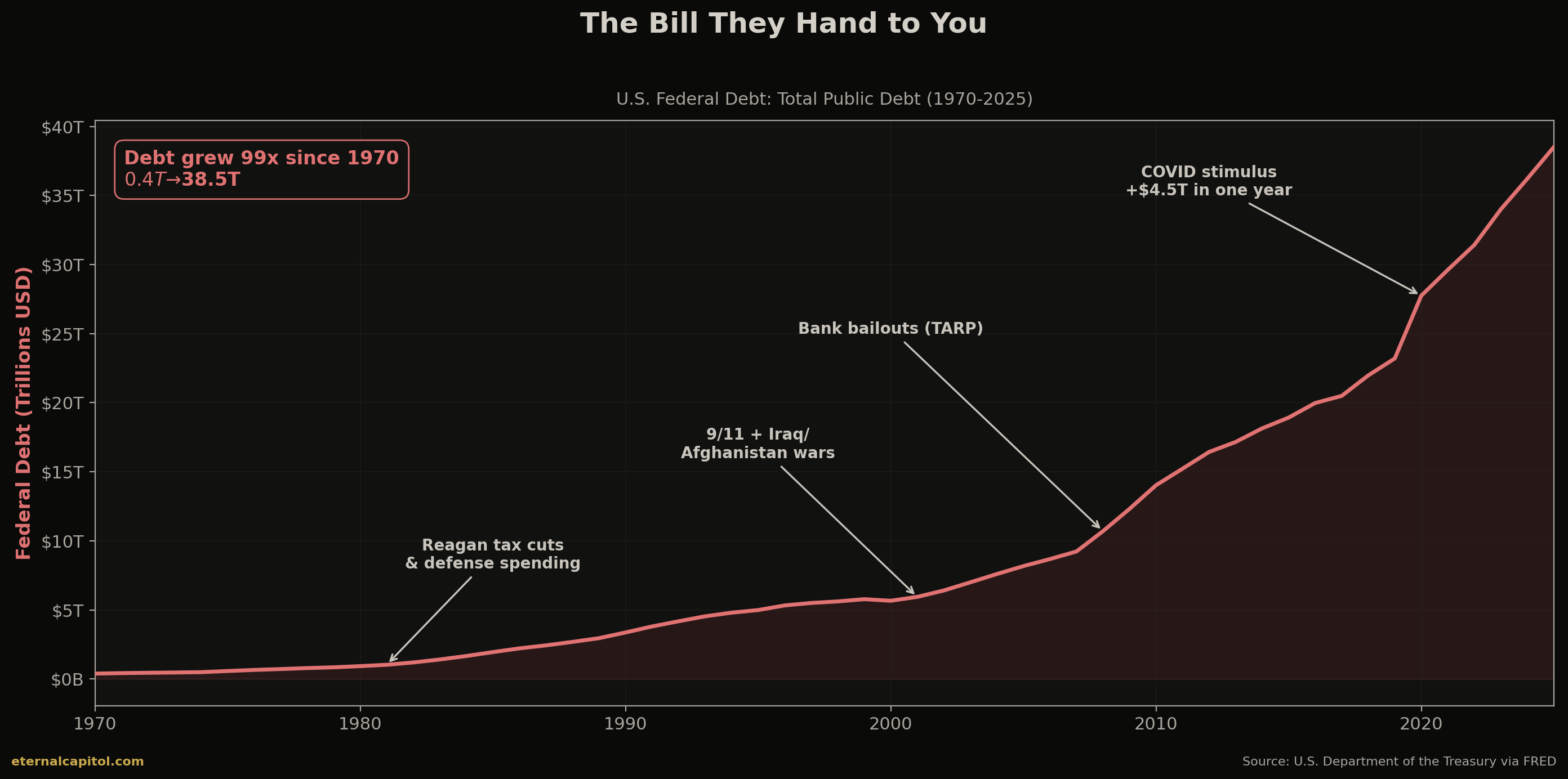

Republicans cut taxes and run up the debt on defense spending. Democrats raise taxes and run up the debt on entitlements. The result is identical: $38.5 trillion in federal debt as of Q4 2025, per the U.S. Treasury. That's 99 times what it was in 1970. Neither party has balanced a budget in over two decades.

Source: U.S. Department of the Treasury via FRED

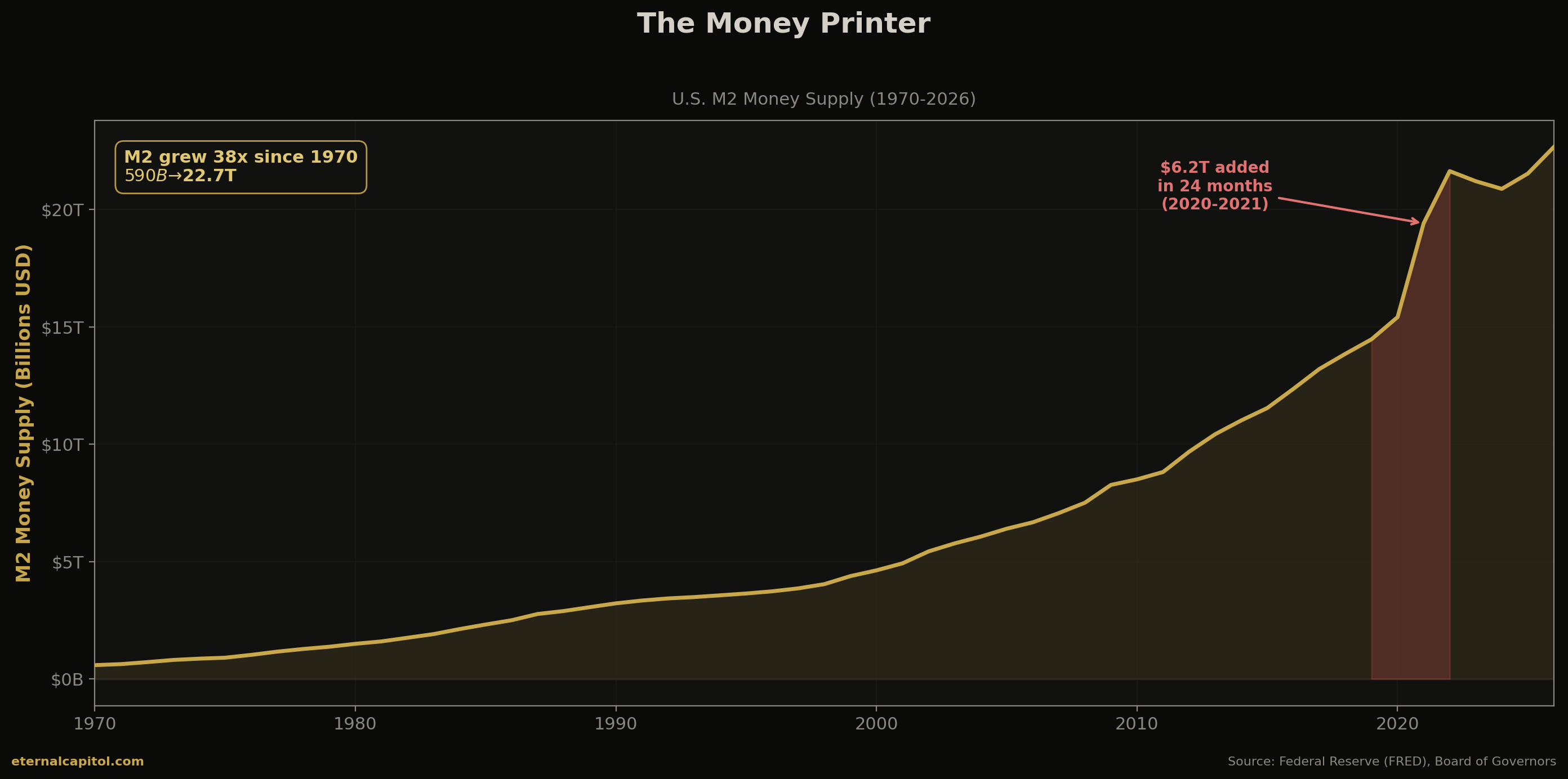

They argue on camera about which programs to fund. Behind the curtain, both sides agree on the one thing that actually matters: keep printing money. Because printing is the only way to service $38.5 trillion in debt without making the hard cuts that would lose elections. The M2 money supply went from $590 billion in 1970 to $22.7 trillion today. That's a 38x expansion, per the Federal Reserve's own data.

Source: Federal Reserve (FRED), Board of Governors

During COVID alone, they added $6.2 trillion to M2 in 24 months. Both parties voted for it. Then they blamed each other for the inflation that followed. Classic.

The Cantillon Effect

Richard Cantillon figured this out in the 1700s. When new money enters an economy, it doesn't spread evenly. The people closest to the source of money creation get to spend it first, before prices adjust upward. By the time that money trickles down to everyone else, prices have already risen. The early recipients bought assets cheap. The late recipients get stuck with the bill.

In practice, this means banks and financial institutions are first in line when the Fed creates new reserves. They buy treasuries, stocks, real estate, corporate bonds. Asset prices go up. The portfolio class gets richer. Six months later, your grocery bill catches up. Your rent catches up. Your wages don't.

This isn't a conspiracy theory. It's the stated design of monetary policy. The Fed targets 2% annual inflation on purpose. They are openly telling you they intend to make your savings worth less every year. And 2% is the target. CPI hit 9.1% in June 2022 after the COVID money printing binge. That wasn't a bug. It was the Cantillon Effect playing out in real time, exactly as Cantillon described 300 years ago.

Their Products, Their Bailouts

Banks don't offer savings accounts and mortgages out of generosity. Every product they sell is designed to benefit them first. Your savings account pays you 0.5% while they lend your deposits out at 7%. The spread is theirs. The risk is shared. Actually, the risk is mostly yours.

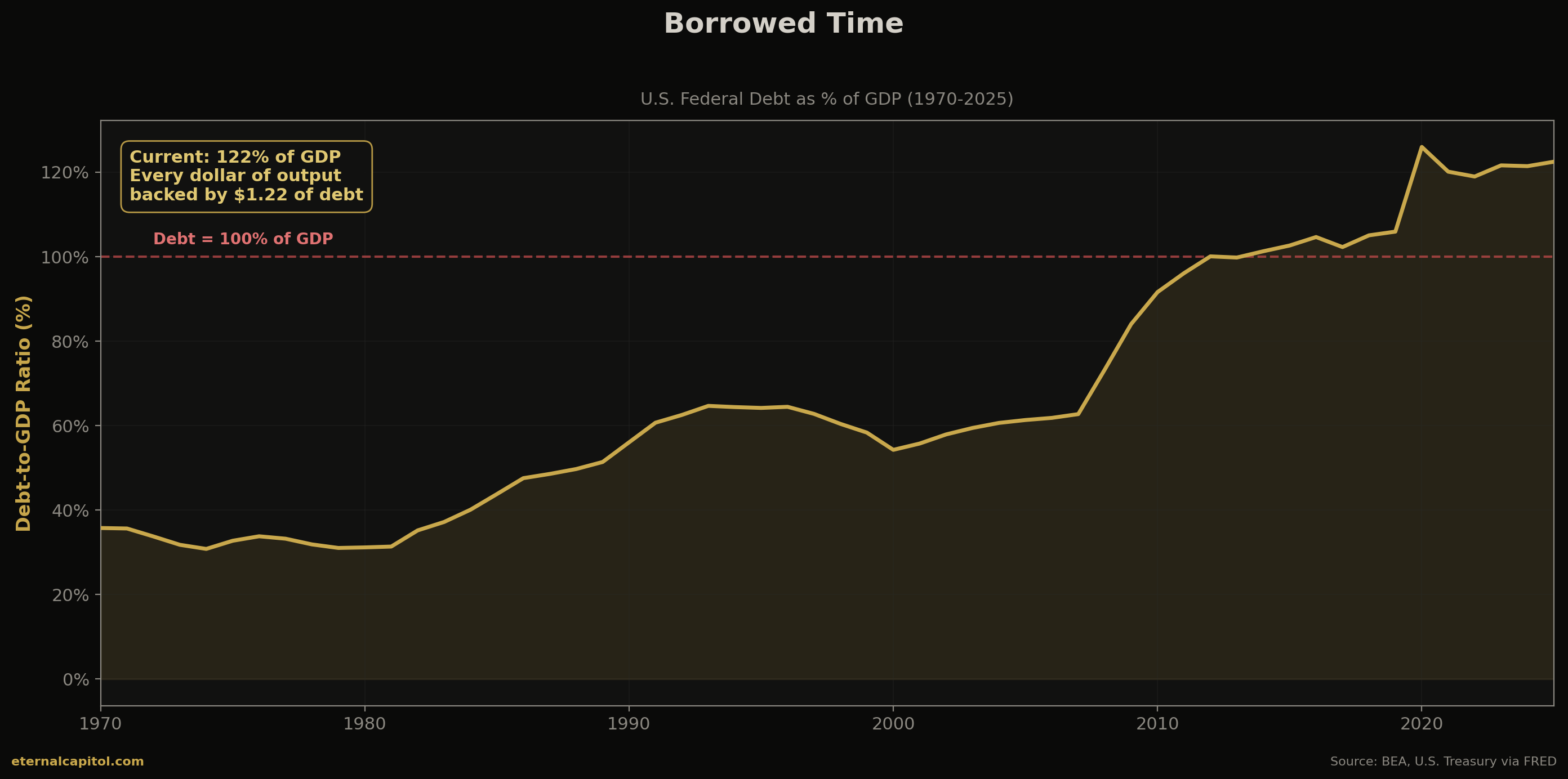

When their bets go sideways, they get bailed out. In 2008, the government handed the financial system $498 billion in direct crisis bailouts, per MIT Sloan's analysis of the Treasury data. The Fed committed $29 trillion in total emergency lending, according to the Levy Economics Institute. Banks got rescued. Homeowners got foreclosed on. Eight million families lost their homes. Then, in 2020, they did it again. Trillions more in emergency lending. PPP loans. Stimulus checks funded by money that didn't exist the month before.

Source: Bureau of Economic Analysis, U.S. Treasury via FRED

Debt-to-GDP now sits at 122%. For every dollar of economic output this country produces, there's $1.22 in federal debt behind it. That ratio was 36% in 1970. The losses get socialized. The gains stay private. Every time.

Ask Yourself the Question

Are you really going to keep transacting in the currency that lets them reap all the benefits while displacing the negatives onto you? They get first access to new money. They get bailouts when their gambles fail. They get asset price appreciation from inflation while you get higher rent and a shrinking paycheck in real terms. The game has been rigged since 1971, and voting for the other team changes nothing about the monetary architecture underneath.

The jig is up. Technology exists now that wasn't available to your parents or grandparents. Bitcoin has a fixed supply of 21 million. No committee can print more of it. No president can executive-order it into existence. No bank can lend it out 10-to-1 and then ask the taxpayer for a bailout when the music stops. It runs on math, energy, and a network that nobody controls.

You can opt out. For the first time in history, you actually can. Self-custody means no counterparty risk. Your keys, your coins, your purchasing power. Not a promise from the same institutions that created the $38.5 trillion hole in the first place.

The greater fool isn't the person who buys Bitcoin. It's the person who keeps holding dollars while every chart, every data point, and every policy decision tells them exactly what's coming next.